Wall Street is currently drunk on the 35% revenue jump at TSMC. The financial press is tripping over itself to scream about "record highs" and "insatiable demand." They see a graph pointing to the top right and assume it represents a healthy, thriving ecosystem. They are wrong. This isn't a victory lap for the semiconductor industry; it is a giant, flashing warning sign of a monoculture that has forgotten how to innovate beyond a single, bloated use case.

TSMC’s record revenue isn’t a sign of strength. It is a tax on desperation. Read more on a related subject: this related article.

The narrative suggests that the Taiwan Semiconductor Manufacturing Company is the engine of the future. In reality, it has become the bottleneck of the present. When one company controls the vast majority of the world’s advanced logic chips, we don’t have a market. We have a hostage situation. The 35% revenue spike isn't driven by a diverse array of brilliant new products; it’s driven by a herd of companies all trying to buy the exact same insurance policy: high-bandwidth memory and massive GPU clusters.

The Margin Trap and the Illusion of Growth

Analysts love to talk about "strong AI demand" as if it’s a permanent fixture of the physics of business. It isn't. What we are seeing is the final, frantic expansion of a bubble built on the back of brute-force computing. Additional journalism by Financial Times delves into related perspectives on this issue.

Companies are pouring billions into $30,000 to $40,000 chips because they are terrified of being the only ones without them. TSMC is simply the house in a casino where everyone is betting on the same color. Their revenue is skyrocketing because they are the only entity capable of printing the chips that fuel this FOMO-driven CAPEX.

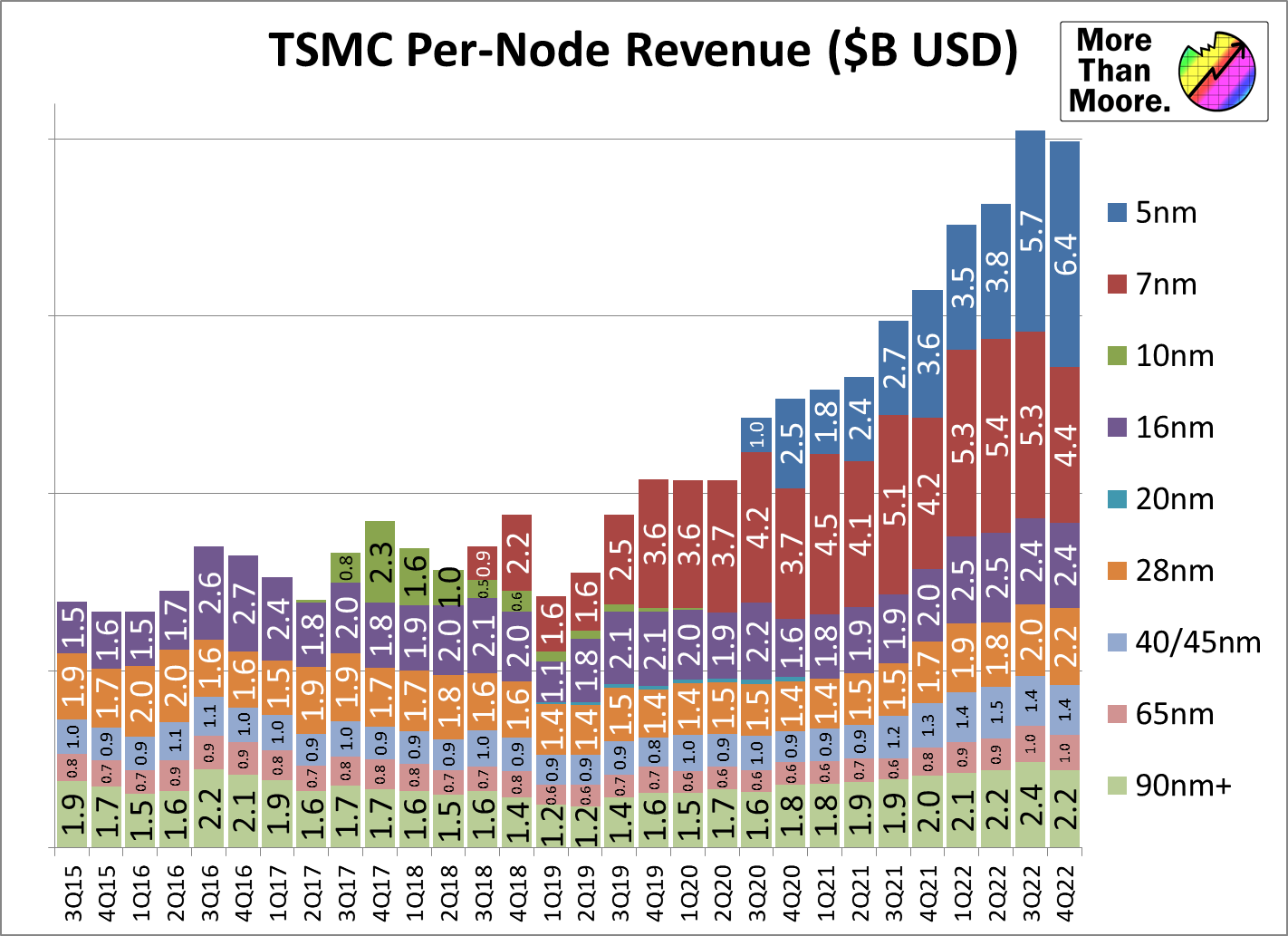

But look closer at the unit economics. The cost of producing these sub-5nm chips is escalating at a rate that the average consumer or even the average enterprise cannot sustain long-term. We are hitting the wall of "Economic Moore’s Law." While it is still technically possible to cram more transistors onto a piece of silicon, it is becoming financially ruinous to do so for anything other than a handful of hyperscale cloud providers.

The "lazy consensus" says that as TSMC scales, costs will drop. Historical data proves the opposite. A 3nm wafer is exponentially more expensive to produce than a 7nm wafer. This creates a barbell economy where you have "God-tier" AI chips at the top and stagnant, lagging-edge silicon for everything else. This isn't progress. It’s a distortion.

The CoWoS Bottleneck is a Structural Failure

The "experts" are currently obsessed with CoWoS (Chip on Wafer on Substrate) packaging. They treat it like a secret sauce. It’s not. It’s a patch for the fact that we can’t make monolithic chips any bigger without them breaking.

TSMC’s revenue jump is largely tied to their ability to provide this advanced packaging. But relying on a single point of failure in the global supply chain for advanced packaging is strategic suicide for the industry. I’ve watched hardware teams spend eighteen months designing a chip only to be told they can’t get packaging slots for two years because a certain three-letter company in Santa Clara booked the entire line.

This scarcity creates a false sense of value. When demand is artificially inflated by supply constraints, revenue looks "strong." In truth, the industry is starving for alternatives that don't involve begging C.C. Wei for a seat at the table.

Why Your "AI Strategy" is Just a TSMC Subsidy

If you are a CEO bragging about your "AI-integrated roadmap," you are actually just telling your shareholders that you’ve found a new way to funnel your cash directly to Hsinchu.

The current crop of AI chips—the ones driving TSMC's record-breaking quarters—are remarkably inefficient. We are using a sledgehammer to crack a nut. The industry has settled on a "more is more" philosophy: more parameters, more power, more silicon area. This is the path of least resistance. It is intellectual laziness.

Instead of optimizing code or finding new architectures that don't require 700 watts of power per chip, the industry has decided it’s easier to just throw money at TSMC. This creates a feedback loop where software becomes more bloated because the hardware can handle it, and hardware becomes more expensive because the software requires it.

The Real Risks Nobody Mentions

- The Single-Point Failure: If a single geography handles 90% of the world's most advanced chips, the "revenue jump" is irrelevant compared to the systemic risk.

- The Inventory Hangover: We’ve seen this movie before. In 2021, the world couldn't get enough chips for cars and appliances. By 2023, there was a massive glut. AI chips are not immune to the laws of supply and demand.

- The Talent Drain: Innovation is being sucked out of other sectors—automotive, medical, IoT—and redirected into making slightly faster Large Language Models.

The Counter-Intuitive Truth About "Record Profits"

High revenue at the foundry level often precedes a massive correction in the end-market. When TSMC reports a 35% jump, it means the input costs for every other tech company just went up.

Unless these companies can find a way to monetize AI at a level that justifies these insane chip prices, their margins will eventually crumble. We are currently in the "spending" phase of the cycle. The "earning" phase is nowhere to be found. Outside of a few cloud providers renting out compute, who is actually making a profit on AI?

The answer is almost no one.

TSMC is the only one consistently winning because they are selling the shovels during a gold rush where nobody has found any gold yet. They are the only ones with a guaranteed ROI. For everyone else, that 35% revenue jump is an expense line item that is eating their future.

Stop Asking if TSMC Can Keep Growing

The question isn't whether TSMC can sustain this growth. The question is: why are we allowing the entire global economy to depend on a single company’s ability to etch patterns on silicon?

The obsession with TSMC’s quarterly earnings is a distraction from the real problem: the death of hardware diversity. We have traded resilience for efficiency, and we have traded innovation for scale.

If you want to know where the industry is actually going, stop looking at the revenue total. Look at the power density and the yield rates. Look at the fact that we are nearing the physical limits of what silicon can do. The 35% jump isn't the start of a new era; it’s the peak of the old one.

The industry doesn't need more "record-breaking" quarters from a monopoly. It needs a total rejection of the "bigger is better" compute model. It needs a move toward decentralized fabrication and architectural shifts that don't require the GDP of a small country to tape out a chip.

The "AI demand" everyone is cheering for is actually a tax on the future of computing. And right now, TSMC is the only one collecting.

Stop celebrating the monopoly. Start fearing the stagnation it represents.

Buy the shovel-seller if you want a safe trade, but don't mistake a crowded trade for a revolution.