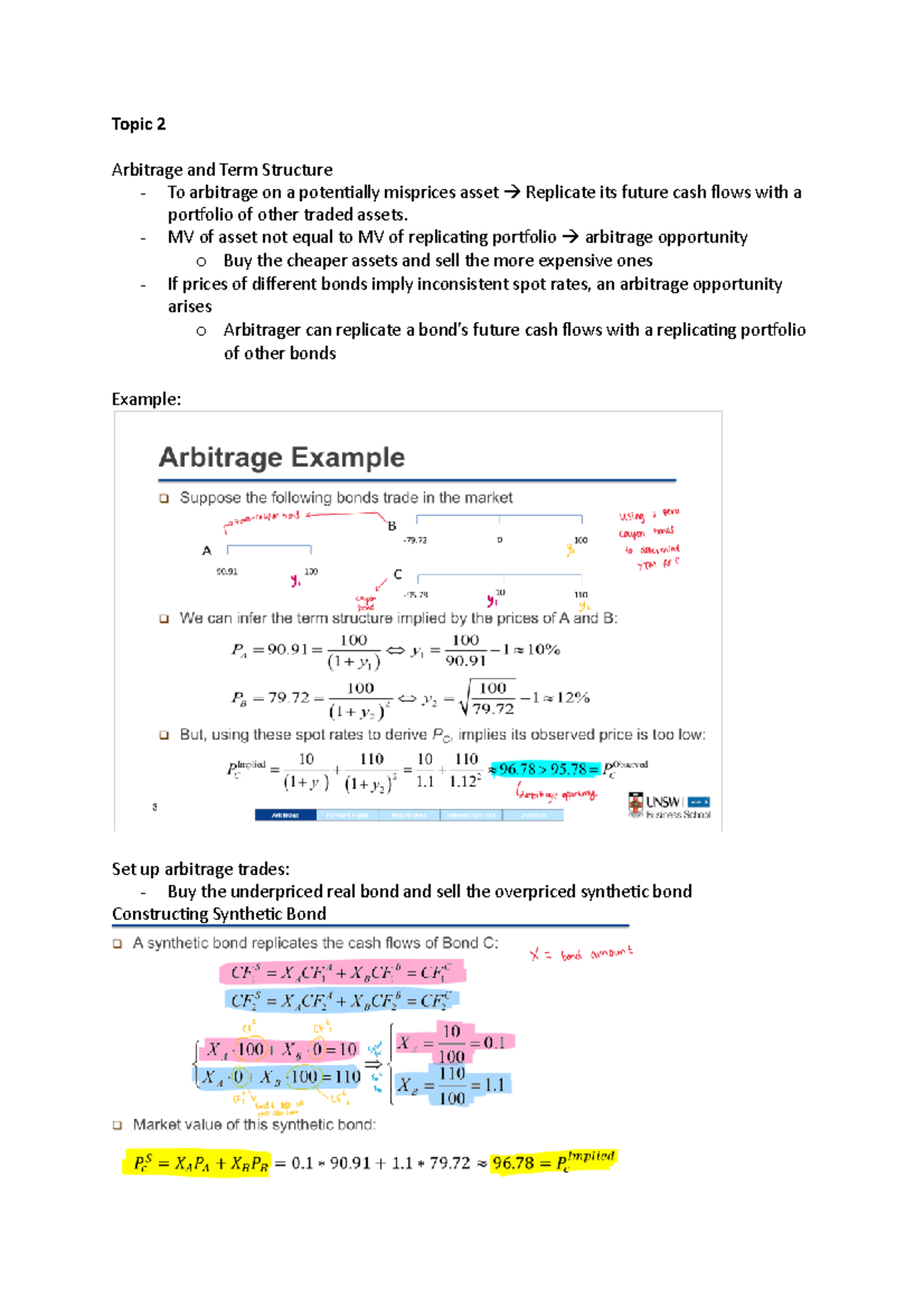

Central bankers usually spend their final weeks in office packing boxes and giving polite, forgettable speeches. Luis de Guindos is doing neither. As the European Central Bank (ECB) Vice-President prepares to step down at the end of May 2026, he's just dropped a massive reality check on those betting on a June interest rate hike. While markets were practically pricing in a move to combat the inflation spike from the Iran conflict, de Guindos is telling everyone to take a breath.

The timing of his warning is critical. We're seeing a tug-of-war between rising energy costs and a growth engine that’s starting to cough and splutter. In his latest discussion with the Financial Times, de Guindos made it clear that he’s moved from the hawk camp to the side of "prudence." He isn't just being cautious; he's worried that the ECB is about to repeat old mistakes by ignoring how fast growth can vanish when energy prices explode.

The growth trap nobody wants to see

The standard central bank playbook says when energy prices go up, you raise rates to stop that inflation from sticking. But de Guindos is pointing to a different set of numbers. He's seeing a drop in consumer sentiment that hasn't fully hit the official reports yet. When people feel poorer because their gas bills are soaring, they stop spending. That kills demand faster than a rate hike ever could.

He’s warned that growth data over the coming weeks probably won't be good. It’s a classic squeeze. If you raise rates into a slowing economy, you don't just fight inflation; you might accidentally trigger a recession. For de Guindos, the impact on growth is going to become much more visible very soon. He doesn't want the ECB to be the ones who pushed the economy over the edge on his way out the door.

Why 2026 isn't 2021 all over again

A lot of people are looking at the current energy shock and thinking it's a rerun of the post-pandemic mess. It's not. De Guindos was very direct about this: back in 2021, we had negative interest rates and governments were throwing money at everyone. Today, we've got positive rates and the ECB is actively shrinking its balance sheet.

We aren't starting from a place of "free money" anymore. The current situation is much more fragile. He even admitted that the ECB was too late to act in the past because they spent too much time in "academic discussions" about whether inflation was supply-driven or demand-driven. This time, he doesn't want to get stuck in a theory. He wants to see the actual hard data from the Iran conflict before committing to a move in June.

The infrastructure scar and the Iran factor

The conflict in Iran isn't just about the price of a barrel of oil today. De Guindos mentioned that even if a truce happens tomorrow, the damage is done. Physical infrastructure has been destroyed. That means the supply side of the economy has taken a permanent hit that interest rates can't fix.

You can't "interest rate" a broken pipeline back into existence. This is where his argument for prudence gets its teeth. If the problem is that there isn't enough energy because of a war, making it more expensive for a bakery to take out a loan won't bring the energy back. It just makes the bakery go bust faster.

Market calm vs. central bank reality

It’s actually kind of weird how calm the markets have been. Credit markets and sovereign bonds haven't panicked yet. They're betting on a "benign scenario" where the war is short and we skip a recession entirely. De Guindos thinks this calm is a good thing—it prevents a financial meltdown—but he isn't buying the optimism yet.

He’s looking at the "Strait of Hormuz" factor. If that shipping lane stays messy, the "benign scenario" goes out the window. His parting shot to his colleagues is basically: don't let the market's current mood trick you into thinking the coast is clear.

What this means for your money

If you're waiting for the ECB's June meeting, don't assume a rate hike is a done deal anymore. Other governors like Joachim Nagel are still pushing for it, but the Vice-President's "prudence" stance carries weight. It suggests a growing split inside the Governing Council.

For businesses and investors, this means the era of predictable rate moves is over. We’re back to "meeting-by-meeting" uncertainty. The smart move right now is to keep a close eye on those growth indicators and consumer confidence surveys de Guindos mentioned. If they continue to slide, the hawks might have to eat their words and keep rates exactly where they are.

Stop looking at the inflation prints in isolation. Start looking at the people. If they're scared to spend, the ECB won't need to raise rates to cool the economy—the energy bills are already doing that job for them. Don't get caught on the wrong side of a policy shift because you ignored the growth warning.