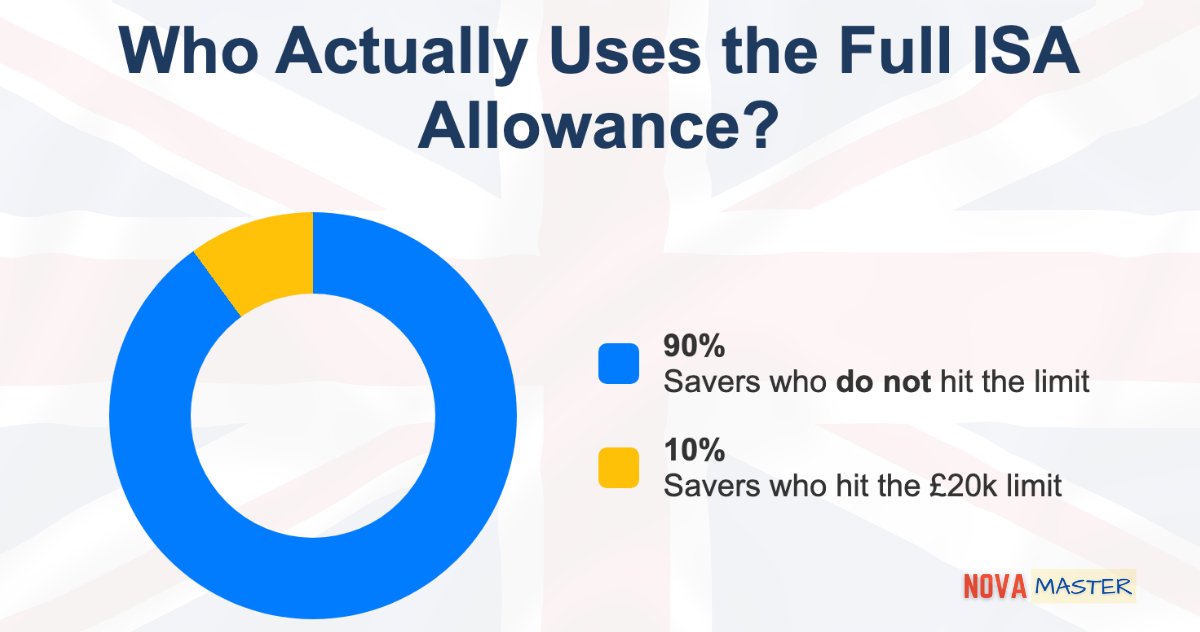

The narrative surrounding the 2026 ISA season has been framed as a flop, a moment where British retail investors collectively turned their backs on the stock market. This assessment is not merely inaccurate; it is fundamentally lazy. The truth is far more complex than a simple loss of interest. We are witnessing a quiet, defensive migration of capital driven by a decade of economic instability and a growing distrust in the mechanisms of wealth creation.

Retail investors are not necessarily fleeing the market out of fear alone. They are reallocating. The reality of 2026 is that the traditional allure of equities has been eclipsed by the immediate, visible comfort of cash.

Why is this happening now? For years, the promise of the stock market was built on the foundation of consistent growth and reliable dividend income. That foundation has cracked. Persistent inflationary pressures have eroded the purchasing power of the average household, forcing a shift in priority from long-term wealth accumulation to short-term liquidity. When the cost of living dominates every financial decision, the prospect of locking capital into a volatile asset class becomes a luxury that many feel they can no longer afford.

The Myth of the Financial Illiterate

Industry analysts frequently cite "financial illiteracy" as the primary reason for low engagement. This is a patronizing explanation. The average UK saver understands the basics of inflation and interest rates perfectly well. They have been living through the consequences for years. They see that cash, while technically losing value in real terms over long horizons, currently offers a predictable return that feels safer than the unpredictable swings of the FTSE 100 or global tech indices.

This is a rational response to an irrational economic environment. If a household has an emergency fund that is struggling to keep pace with rising costs, every pound directed toward an ISA is a pound that cannot be used to cover the next unexpected expense. The decision to shun stocks is not a lack of knowledge; it is a calculated risk management strategy.

The Complexity Trap

The government’s attempts to stimulate retail investment have paradoxically created more friction. By introducing complicated tiering, proposed changes to allowances, and shifting tax treatment for different vehicles, policymakers have added layers of administrative burden that confuse the average user.

Consider the hypothetical scenario of a middle-income earner weighing their options. They see a confusing array of Cash ISAs, Stocks and Shares ISAs, and emerging alternative products. Each comes with a different set of rules, tax implications, and risks. The mental energy required to navigate this mess is often greater than the perceived benefit of the potential returns. When the system itself is an obstacle, it is no surprise that individuals opt for the path of least resistance: the standard high-street savings account.

Home Bias and the Search for Familiarity

There is a distinct preference for domestic stocks among British investors, yet the performance of the local market has often disappointed those seeking aggressive growth. This creates a psychological barrier. Investors look at their own country’s market, see stagnation or slow growth, and compare it against the high-octane performance of US tech giants. The result is a feeling of being left behind, which manifests as disillusionment.

Yet, even when they look abroad, they are met with the volatility of a global economy marred by geopolitical tension. The fear of being exposed to a cyclical downturn—or a sudden shock—is acute. Investors are seeking "safe havens" in a world where those havens are increasingly difficult to define. They are looking for companies that provide the basics of life: utilities, consumer goods, and essential services. These are not exciting, disruptive companies. They are the bedrock of a stable economy, and for many retail investors, they are the only things that feel "real" enough to justify an investment.

Structural Failure of the ISA Brand

The ISA, once the crown jewel of British personal finance, is suffering from a branding crisis. It is marketed as a vehicle for wealth, but it is often used as a glorified savings bucket. The transition from a tax-efficient home for investments to a flexible, liquid container for cash has weakened its purpose.

If the objective is to create a nation of investors, the current approach is failing. We need a fundamental rethink of how these products are presented. It should not require a financial degree or a weekend of research to understand why one might choose an equity-based fund over a cash deposit.

The industry is currently obsessed with "product innovation" when it should be focused on "system simplification." As long as the entry barrier remains high—not in terms of capital, but in terms of cognitive load—retail investors will remain on the sidelines.

The data from the end of the tax year, while showing some movement toward global equity trackers and specific investment trusts, reveals a concentrated interest. Those who are still playing the market are not doing so with broad, confident strokes. They are playing with extreme caution, favoring defensive positions that offer a semblance of security.

This is not a temporary dip in enthusiasm. It is a long-term shift in the relationship between the British public and their financial institutions. If the goal is to reverse this trend, the industry must stop blaming the investors and start addressing the structural, psychological, and economic realities that have made the market a place to avoid rather than a place to grow.

The silence from retail investors during this ISA season is not an accident. It is a loud, clear message that the current system is not working for them. Until that is acknowledged, and until the friction is removed, the market will continue to be a playground for the wealthy and a source of confusion for everyone else.

The clock is ticking on the next tax year, and the same patterns are set to repeat unless the fundamental disconnect is addressed. Confidence is not something that can be manufactured through marketing campaigns or government incentives; it is earned through stability, simplicity, and results. Right now, none of those factors are present in a way that resonates with the average person.